#11 Weekly market update (28/11/2021 - 03/12/2021)

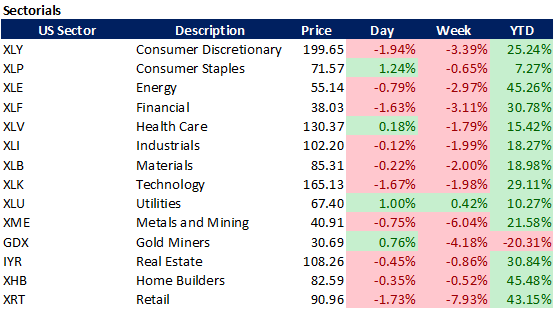

Weekly performance:

Key takeaways:

Economic calendar. The Royal Bank of Australia is expected to announce its interest rate decision, which is expected to remain at 0.10%. The UK’s Halifax House Price Index and German ZEW Economic Sentiment will be released on Tuesday. All eyes will undoubtedly be on the US’ CPI data for the month of November. A higher-than-expected reading would spike volatility while inflation coming lower could favour the positive gamma. Unit labour costs, trade balance and nonfarm productivity will also be published. Japanese GDP growth and Chinese trade balance data may drive the direction of Asian markets. In Europe, Lagarde is expected to give a press conference on Wednesday. US Crude Oil Inventories may lead the black gold to rebound after its devastating month.

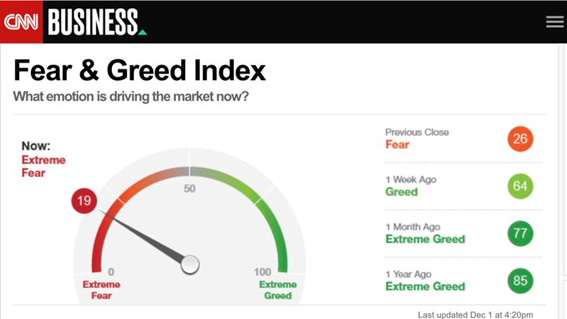

Macroeconomic outlook. Omicron variant’s coverage was five times that of the Delta’s. Powell and Yellen admit inflation not to be transitory as disruptions persist. University of Michigan’s Consumer Sentiment Index reaches a new decade low. Buying Condition Indexes hits a new historic low. CNN’s Fear & Greed Index on “Extreme Fear”. Italian Services Business Activity Index contracts to 17.4, the lowest since January 1998.

Equities. 26th Nov. registered $2.04bn inflow on US Stocks by retail investors, the second biggest day ever. Major indexes registered losses during the last trading week as divergences and scientific uncertainties with regards to the new variant remain. December tends to be a favourable month for the S&P 500, which is currently fighting against its 100-MA. Charlie McElligott from Nomura expects volatility to remain high until the option expiry date, warns of possible CTA sell-off below $4,496, which would re-activate exposure to fat tail risks.

Fixed Income. The US yield curve resumes its flattening, anticipating a Fed’s policy mistake. Hedge funds’ net shorts on US 30Y Treasuries at the lowest since January 2019. Hedge funds’ net shorts on US 10Y Treasuries at the highest since February 2020. Massive inflows on the $TLT ETF, increasing exposure to 20Y+ Treasuries.

FX. South African Rand plummets 6% against the USD month-to-date. Historically, December is a seasonally unfavourable month for the greenback for fiscal reasons, but the macroeconomic scenario may break this seasonality. Swiss Franc (CHF) reaches a new high since July 2015, re-activating its hedging role.

Emerging Markets. Chinese Developer Evergrande warns that it may run out of money. TRY/USD hits a new low after the Turkish President fires the Finance Minister.

Commodities. November has been the worst month for Crude Oil since the beginning of Covid-19, with a -15% return MTD. OPEC announces plans to increase oil supply in January despite the recent plunge. Lumber soars 18%, favoured by seasonality.

Omicron variant spikes volatility and Powell admits inflation is not transitory

As we analysed in #10 Weekly Market Update, the Omicron variant hit headlines and triggered a sell-off, which was intensified by the lack of liquidity as a consequence of the US Thanksgiving holiday. Actually, Bloomberg has compared the number of mentions of this new variant to these of the Delta and, as we can observe in Figure 1, Delta was nowhere near as trendy as Omicron. In the previous post we analysed some divergencies which suggested end-of-month portfolio rebalances or simply rotations across sectors were distorting the Friday’s trading session, whomst shifts were amplified by the low liquidity. Vanda Research also identified how Friday’s Omicron sell-off witnessed the second biggest day of net retail buying of US stocks on record ($2.04bn). As we can see in Figure 2, Friday’s volume was similar to that after the Delta sell-off in July where the retail crowd also jumped on the bandwagon to catch some bargains. Figure 3 depicts the Dark Pool Index, which has shown contradictory lectures during the whole week. Nevertheless, the MoC Indicator is reflecting a predominance of a bearish sentiment (See Figure 4).

As we can see in Figures 5 & 6, the week opened with the SPX recovering half of the losses from Friday’s sell-off. In case of the NASDAQ, it had already yielded some returns before Monday’s closing. Nevertheless, the Tuesday session opened with the CEO of Moderna claiming that the vaccine would be much less effective against the Omicron variant. He added that it may take months since a new vaccine, which specifically targets the new variant, is developed and shipped. As soon as the news were published, the S&P 500 futures plummeted 133 bps in less than half an hour. Yet, the panic progressively decreased when other institutions like Pfizer, Oxford, WHO and the Israel’s Minister of Health released several reports contradicting Bancel’s statement. On the following day, the Federal Reserve Chairman Jerome Powell responded to questions of the Senate Committee on Banking, Housing and Urban Affairs. During the session, several Republican members grilled Powell on inflation-related questions. After several questions, Pat Toomey, a Republican from Pennsylvania asked: “How long does inflation have to run above your target before the Fed decides, maybe it’s not so transitory?” It was then when, to everybody’s surprise, Powell admitted that the time has come to stop referring to the inflation as transitory. Mike Crapo, another Republican from Idaho put the Chairman against the ropes when asked whether the Fed’s would modify the proposed tapering process as well as the timing of the rate hike given the Omicron variant news. Overcome by the massive inquiries, he suggested the Fed’s bond-buying program would be brought to an end sooner than expected. Moreover, he left the door open to raising interest rates sooner. The final decision will be announced at the next meeting scheduled for December 14-15th. Powell also stated that the recovery of the US economy has been sharper than that of other economies as a consequence of the more solid fiscal stimulus. While the retail sales soared during the month of October and the unemployment level reached the lowest in the last 52 years, last week’s University of Michigan Consumer Sentiment Index reached a new decade low (Refer to Figure 7). Similarly, the Buying Condition Indexes reached a new historic low (See Figure 8). In Figure 9 we can observe how the inflation expectations remain at the highest level since 2008. It was when Powell was asked about the increasing inflationary pressures that he admitted that the risk of higher inflation has increased. While some months ago, the narrative was that about 60% of the price increases were being caused by “transitory effects” related to Covid-19, Jerome Powell concluded the meeting by stating “I think what we missed about inflation was that we didn’t predict the supply-side problems, and those are highly unsual and very difficult, very non-liner, and it’s really hard to predict those things, but that’s really what we missed, and that’s why all of the professional forecasters had much lower inflation projections”. Immediately after the panel, markets reacted sharply initiating a domino effect.

As always, the first movers were fixed income traders, who resumed its flattening strategy. As we can see in Figure 10, the US 10Y Treasuries are slumping while the US30Y Treasuries are soaring. This divergence is even greater when comparing the US 30Y against the US 5Y. According to the economic theory, under “normal” circumstances, when US 10Y Treasuries fall X%, US 30Y Treasuries should respond by decreasing 3X%. Said in other words, fixed income traders are currently pricing their distrust on the Fed. By executing this trade their message to the market is that the Fed will make a policy mistake if they hike rates as bond investors are currently estimating the Neutral Rate of Interest to be around 0.4%, which means that the Fed has an insignificant margin of safety when raising interest rates. To put it simple, were the Fed to hike rates, they would have no choice but to lower them in the following months. As usual, hedge funds have already spotted this trend and, as we can appreciate in Figure 11, they have significantly increased their short positions on the US 10-year Treasuries, being the shortest since February 2020. Similarly, we should complimentarily use Figure 12 in order to identify the flattening trade. In this graph we can observe how the hedge funds are also undoing its short positions in the US 30-year Treasuries, which are expected to become net-long in the next weeks.

Figure 13 shows the technical chart of the $TLT, which is an ETF which replicates 20+Year Treasury Bonds. As we can observe, the considerable inflows in this security can be explained by the abovementioned reasoning. Yet, not all that glitters is gold. American High-Yield Bonds registered the highest outflows ($4,200 million) in the last eight months as a consequence of a higher likelihood of the Fed hiking rates sooner than expected as well as the unexpected Omicron variant (Refer to Figure 14). Other analysts attributed the drawdown to the characteristic lower risk tolerance by end-of-year. With regards to the MOVE Index, which captures the movement in US Treasury yield volatility implied by the current prices of one-month OTC options on 2-year, 5-year, 10-year, and 30-year Treasuries, it has tripled YTD (See Figure 15).

Another indicator of the widespread panic is the CNN’s Fear & Greed Index, which has shifted from Greed to Extreme Fear in less than a week (See Figure 16). It is worth mentioning the screenshot was taken on December 1st to capture the volatility currently driving markets. As of December 3rd post-closing, the indicator accounts for 20 – Extreme Fear.

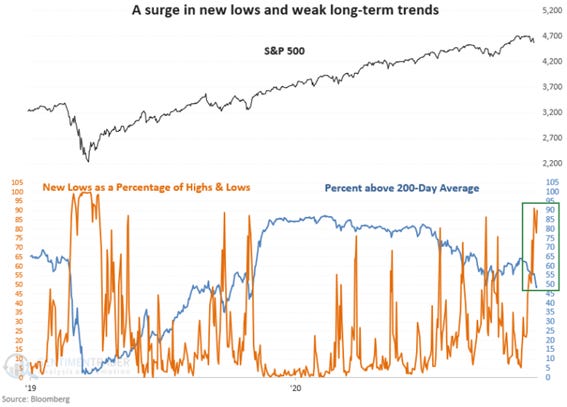

As of this writing, the divergences in the major indexes are increasingly evident. As observed in Figure 17, the S&P has been steadily increasing. Nevertheless, the percentage of stocks over its respective 200-MA has sharply decreased while the number of new-lows has skyrocketed during the last month.

During this week, several quant analysts, among whom we can find Charlie McElligott from Nomura, expect volatility to remain high until the option expiry date (≈December 17th). The renowned analyst from the Japanese investment bank has observed that a massive drawdown would take place if the CTAs sold their shorts given the quantitative market structure would significantly deteriorate and in turn, volatility would skyrocket, triggering a massive selling pressure. All this combined, would re-activate a hypothetical exposure to fat tail risks, or, said in other words, a 3σ-correction which probability of occurrence equals 0.3%. According to him, this would happen if the spot of the S&P 500 drops to $4,496, where CTAs would go from 100% long to ≈40% short. We must bear in mind that CTAs do normally trade with futures and when they change their positions, they would have completed their “trade” in less than 24-48h. As we can observe in Figure 18, the $4,496 level is close to the SPX’s 100-MA, precisely the same point at which it rebounded on Thursday.

Other investment banks have also given their opinion about the impact of the Omicron variant on financial markets. If we recall from November’s BofA Global Fund Manager Survey, only 5% of the respondents believed Covid-19 to be a tail risk, which implies that 95% of them has been caught red-handed. As we can observe in Figure 19, 65% of them also believed inflation to be “transitory”. In a nutshell, as of this writing we find in a totally different macroeconomic scenario where i) a new Covid variant is threatening the economic recovery of most of the already deteriorated economies and ii) The two spokespersons of the most influential supervising and regulatory financial institution have recently admitted that we should stop referring to current inflation as “transitory”.

According to Bank of America, the base scenario now comprises a marginal risk of correction from the prior forecast. Nevertheless, they believe the political aversion to tough restrictions as well as well as the rapid vaccine deployment should have little or no effect on consumption patterns. When it comes to the monetary policy, they state that a hypothetical spike in contagions could impact demand, which would in turn affect the supply side by the economic activity interruptions. Consequently, the inflationary pressure would accentuate and, given central banks are already pushed to cope with high inflation levels, which could translate into a more aggressive monetary policy or, what is the same, higher real yields for bonds. They also advise that should the “slow growth” narrative gain predominance over inflationary concerns, the Fed would be forced to delay its hawkish response. Finally, they conclude the paper by providing their bearish sentiment on European equities. By sectors, they underweight cyclicals and the automotive industry. They remain bullish on the financial services industry (banking & insurance).

Kolanovic from JPMorgan, who is probably the most bullish among all major investment banks, recommends buying the dip. After narrating the US Thanksgiving sell-off episode and this week’s controversy initiated by the CEO of Moderna, Kolanovic emphasized that most of their clients were more worried by the governments’ reaction than by the Omicron variant itself. He gave some examples of inconsistent measures across countries: “As of today, we can observe restricted air traffic from several African countries where Omicron has not been identified yet. Meanwhile, other European countries who have already reported new cases from the Omicron variant have not interrupted its scheduled flights. He concluded his speech by citing a scientific paper from Gabriela Gomes, which concludes that when old variants propagate thus mutating into new variants, these turn out to be more infectious but with a significantly lower mortality rate. In order to formulate his hypothesis, he attributes the Covid evolution to be the same to the abovementioned pattern. Thus, following this rationale, he believes that the Omicron variant could progressively be “normalized”, which would bring normality back to markets. Said in other words, he sees this opportunity as ideal to go long on cyclicals, commodities and the so-called “re-opening trade”. Whether he is certain is still unclear given the lack of scientific evidence about the new variant. As the saying goes, the cobbler should stick to his last.

Other banks like Barclays seem not to be that bullish. On the paper published this week they emphasise on the equities’ high valuations, but they still foresee the S&P exceeding the $4,800 level by 2022.

On the Old Continent, the EU PMIs have been released this week and have beaten expectations (See Figure 20). When it comes to the Euro area PMI, the IHS Markit Composite indicator hit 55.8 for the month of November, well above forecasts of 53.2 (vs. 54.2 October). Moreover, as observed in Figure 21, the manufacturing growth in the Eurozone is at the highest level since 2011, accounting for 55.4%. The main negative highlight has been the disastrous Services Business Activity Index reading for Italy, which has contracted to 17.4 (prev. 52.1), the lowest since January 1998 (Refer to Figure 22).

When it comes to European Markets, both the German DAX and the Euro Stoxx 50 are fighting against their respective 200-MA, a crucial technical level (Refer to Figures 23 & 24). Undoubtedly, the most bearish Index is the Spanish IBEX-35, which has already lost the 200-MA (See Figure 25). It is worth mentioning that one deterrent to international investors is the Tobin tax, which was implemented on January 16th, 2020, and consists of a 0.2% tax on share purchases of publicly listed companies with market caps with than EUR 1,000 million. Last month, the Spanish authorities announced revenues of EUR 400 million (vs. 850 million expected). This week, Reuters has conducted a survey to 23 asset managers, who predict that the German DAX and the French CAC would soar 8% and 6% in 2022, respectively with respect to the last Monday’s closing price. When it comes to the Euro Stoxx 600, they foresee the European Index to rise by 7%, 10 bps higher than the all-time high registered on November 17th. Philipp Lisibach, Chief Global Strategist, and the Head of Global Investment Strategy at Credit Suisse, expects a single-digit growth for the next year, compared to the double digit (expected) in 2021. Nevertheless, the negative sentiment to European equities is progressively gaining momentum as there is an increasing risk of higher inflationary pressures, which would force the ECB to accelerate the reduction of its monetary stimulus. Banks, who are extremely sensitive to interest rate fluctuations and cumulate a 28% return YTD, would benefit from increased rate hike expectations.

As for commodities, one of the most affected has been the Crude Oil, which has had a return of -15% MTD, the worst month since the beginning of Covid-19 (Refer to Figure 26). Nevertheless, a lot of water has flowed under the bridge since then (+400% return). The negative momentum started on Friday after the Omicron variant hit the headlines. As a response, the Brent Crude Oil Futures slumped 11.5%, the biggest decline since April 2020. The futures of the WTI Crude Oil perforated the 200-MA. The losses were magnified when the US crude-oil inventories turned out to be lower than expected, but domestic production rose to an 18-month high. While a weakening demand has been observed, some analysts defend that the weekly reduced demand for oil may be related to the US Thanksgiving holiday.

On Thursday, the price of Crude rebounded after the OPEC and its allies announced they would stick with the plans to increase supply in January despite the recent plunge, an announcement which reinforces the Goldman Sachs’ bullishness of Crude. In a recent paper they stated that closing output gaps and eventual pass-through of input price pressures should lift core inflation further in Asia in 2022 (currently higher than consensus), which will be affected by soaring energy prices. As we can see in Figure 27, hedge funds have not changed their view on the black gold and remain net long. The decision surprised most analysts, who were expecting the OPEC to interrupt its output increase of 400,000 barrels per day. In that same statement, the OPEC said that it would continue to monitor the oil market closely and left the door open to immediate adjustments if needed. The next meeting is expected to take place on January 4th 2022. According to estimates from the International Energy Agency (IEA), the OPEC and Russia could account for 58% of the global oil supply by 2050 (vs. 46.5% as of 2020) as a decreasing number of countries (including the US) investing in oil exploration and production in an attempt to reduce its carbon footprint.

December: A seasonally bearish month for the USD but bullish for equities

Macroeconomically speaking, the USD will benefit from the current situation in the world’s largest economy. As commented above, the Fed’s acknowledgment of the inflation not being transitory leads to a faster tapering process and, as a consequence, a sooner-than-expected rate hike. All this combined, favours the greenback, which cumulates a significant outperformance against its peers. As a matter of fact, Nomura released a paper forecasting the EUR/USD at 1.10, which represents a ≈3% decrease from today’s price. Nevertheless, the USD has yielded negative returns in the last trading month during the last five decades (Refer to Figure 28). As we can observe, the seasonality pattern is significantly evident when compared to the rest of trading months. The reason of such an underperformance is merely fiscal-related. Seasonax, the entity specialized in seasonality patterns, confirms that the weakening of the USD during that month is a by-product of the North American tax legislation. As a result, countless US-based companies decide to transfer cash to foreign subsidiaries in order to report a lower amount of USD. This massive outflow leads to an increased demand for foreign currencies, which in turn distorts currency exchanges. As the following year begins, these companies undo the transfer bringing the zero-sum game to an end. Seasonax concludes its paper by advising that the seasonality should never be used as a trading strategy on its own. Actually, since 2000, the USD has underperformed on 17 occasions, breaking the seasonality pattern on the 6 remaining. As of today, hedge funds remain net long in the greenback (See Figure 29).

Conversely, December tends to be a favourable month. As a matter of fact, November and December are the second and third best month for the S&P 500 since 1950 with an average yield of 1.7% and 1.5%, respectively. This year, November has not turned out to be that fruitful as the Omicron variant brought about the world major indexes to plummet. Nevertheless, if we rely on the seasonal component, the S&P 500 has obtained positive returns in December in 74% of the years since 1928, more than any other month. Ryan Detrick, one of the most renowned market strategists from LPL Financial stated that December returns tend to be higher when the SPY has outperformed during the prior eleven months. This may justify the increasing net long positioning of hedge funds on the S&P 500 and the NASDAQ Composite (Refer to Figures 30 & 31)

TRY/USD hits a new all-time low after Erdogan fires finance minister

The Turkish drama remains hitting the headlines as the Turkish Lira keeps depreciating against the USD as a result of Erdogan’s new scene. Last week the Turkish President addressed the nation on a late-night televised programme, positioning himself against hiking rates, a decision which according to him, causes inflation. After the speech, numerous protests given the increasing difficulties to buy staples took place in some of the biggest cities in Turkey. In this week’s reality show, Erdogan fired the finance minister Lütfi Elvan, who had served for one year, and replaced him with Nureddin Nebati. To put things into perspective, Nebati had already served three years as a deputy finance minister and had been trying to implement a policy of low rates, which in the end failed as a result of the strong opposition. Last week, he tweeted: “This time, we are determined to implement it”. Erdogan also said that interest rates would fall markedly until the next elections. As we can observe in Figure 32, the TRY/USD reached a new all-time low of 13.95. The par ended the session at 13.40, hours after the appointment. Year-to-date, the Turkish Lira has lost almost half of its value against the greenback.

Disclaimer: I have done my best to ensure that the information provided on this newsletter is accurate and provide valuable information. Nevertheless, the content is used for illustrative purposes only and does not constitute investment advice.

Before you leave…

I kindly welcome your feedback/suggestions/critics, etc to improve the usefulness of it to you. You can reach me at jramos@u.nus.edu. If you would like to receive the newsletters as they are published please subscribe. I also appreciate if you share it with your friends who are interested in this space. Thank you.