#13 Weekly market update (13/12/2021 - 17/12/2021)

Weekly performance:

Key takeaways:

Economic calendar. After last week’s intervention of some of the major central banks, the RBA is expected to release the latest Monetary Policy Meeting Minutes on Monday. In the wake of the first-rate hike in the last three years, the UK will provide further guidance by publishing November’s retail sales and its GDP growth. The PCE, Conference Board’s Consumer Confidence and the GDP will be some of the most relevant macroeconomic data in the US.

Macroeconomic outlook. 55% of the BofA’s Global Fund Manager Survey respondents claim inflation to be transitory, consider central bank rate hikes to be the biggest threat. The Fed doubles the pace of tapering to $30bn a month, leaving the door open to 3 interest rate hikes in 2022. The Fed balance sheet currently accounts for $8.7 trillion in assets, more than twice with respect to March 2020. US PPI reading shows an increase of 9.6% YoY, the highest since 2010. November’s US retail sales show a cooling down in consumer sentiment, suggesting the economy may not be ready for rate hikes. UK’s CPI reaches a 10-year high at +5.1% YoY and the BoE reacts by increasing rates by 0.15%, to 0.25% after a majority of 8-1. The ECB announces the scheduled PEPP and APP for 2022, which are considered of vital importance to reinforce the accommodative impact of its policy rates and expects no rate hikes throughout 2022. Mainly distorted by soaring energy prices, Germany’s PPI reaches a 56-year high.

Equities. The heightened alert in the UK brings about panic sentiment in financial markets, with travel-related stocks plummeting by more than 3%. The S&P 500 rebounds exactly on the $4,642 technical level, the flip dealer point. The NASDAQ Composite, among the worst performers of the week (-2.95%) as a result of the massive exodus from unprofitable tech and software companies with an EV/Sales ratio of at least 8x. The lack of liquidity magnifies volatility in Friday’s options expiry date as asset managers rebalance their portfolios for the end of the fiscal year.

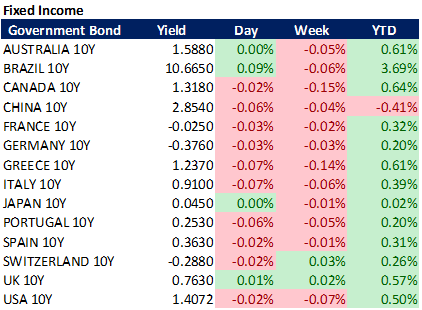

Fixed Income. BofA’s Global Fund Manager Survey shows a significant inflow in bonds, something which did not occur since early 2021.

FX. The greenback’s net long positions reach the highest since mid-June 2019 after 21 consecutive bullish weeks.

Emerging Markets. Turkey’s Central Bank cuts rates again for the third month in a row, Turkish Lira plummets and breaks the psychological barrier of 15 TRY/USD. The MSCI Turkey ETF reaches an all-time low at $16.97. The Hang Seng Index currently trades below book (P/B = 0.99). After the default of Evergrande, the Swiss private bank Lombard Odier attributes a 30% default rate in the offshore USD China high yield real estate market, shifting from idiosyncratic risk to a systematic one.

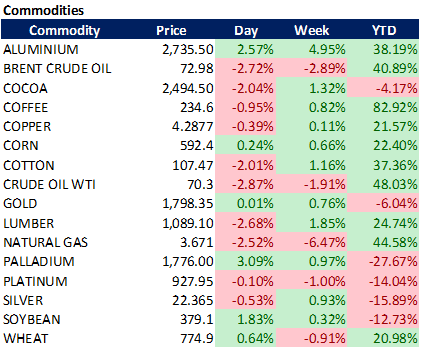

Commodities. Goldman Sachs forecasts crude oil to reach $100 per barrel by 2023 amid massive demand in the next two years.

BofA’s Global Fund Manager Survey shows interesting findings

BofA has recently published its monthly survey to 371 fund managers, with a combined $1.1 trillion in AUM. Despite the results representing a mere opinion, some interesting facts may be observed.

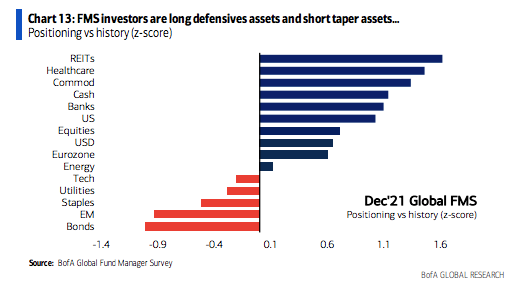

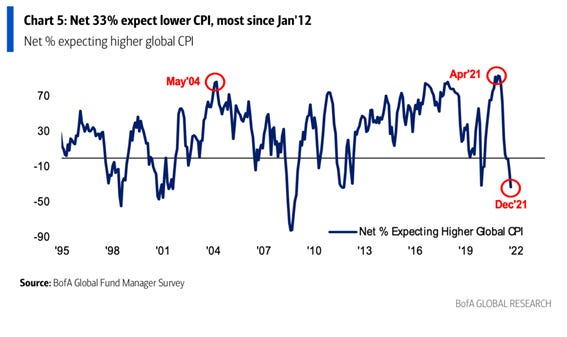

First, the levels of cash have reached their highest since May 2020. Throughout 2021 fund managers have been piling up cash as the S&P 500 increased, and as we can observe in Figure 1, the average cash balance has exceeded 5% in December (vs. 4.4% prev.), reinforcing the hypothesis that the latest bull run has been sustained thanks to both corporate buybacks and retail investors. When it comes to positioning, the sampled institutional investors have reported a clear rotation to defensives, such as Healthcare and utilities. Surprisingly, there has been a significant inflow in bonds, something which did not occur since early 2021 (Refer to Figure 2). Figure 3 shows the percentage of asset managers overweighting equities (LHS) and that of these expecting a stronger economy (RHS). As observed, these variables have been historically highly correlated, except for this year, when growth forecasts have suffered a significant drop while exposure to equities remained close to all-time highs. This month they have shown correlation again, with only 6% of the sample expecting a recession to take place in the next 12 months. The risk-on trade persists as investors are still long on defensives (healthcare, cash) and pro-inflationary sectors (commodities, banks). At the same time, they also remain underweighting sectors that are sensitive to rate hikes, like bonds or emerging markets (See Figure 4). But the main takeaway from December’s survey is the perception of inflation by institutional investors. As we can observe in Figure 5, there is a greater divergence between opinions as 55% of these believe it is transitory (vs. 61% prev.). Moreover, the percentage of voters has also decreased compared to November (91% vs. 96% prev.), suggesting the debate is still running hot. As for the expected inflation, 33% of the sampled asset managers foresee lower inflation ahead, the most since January 2012 (See Figure 6). Finally, one of the most followed questions is the identification of the biggest tail risks. As appreciated in Figure 7, the number of managers perceiving the central banks’ hypothetical rate hikes as a tail risk has doubled MoM. Similarly, institutional investors pointing at the outbreak of the new Omicron variant as a threat has tripled. Another equally important tail risk is the possible contagion effect of the default of Evergrande and its impact on the financial system. As a result, new perceived risks such as i) Geopolitics; ii) China credit contagion and iii) EM currency crisis may bring about a new period of negative sentiment towards EM.

FOMC Meeting: The Fed doubles the pace of tapering to $30bn a month, leaves the door open to 3 interest rate hikes in 2022

All eyes were on the FOMC Meeting scheduled for Wednesday, December 15th. Despite markets not having excessively reacted to the US CPI reading released last Friday, the Monday session triggered some losses as a result of negative news with regards to the Omicron variant. The heightened alert in the UK has brought about panic sentiment in financial markets, which were caught red-handed when data demonstrating that 40% of the daily cases in London currently belong to the new variant was published. Moreover, The UK Health Security Agency announced that same day that they had registered its first death of a patient with the Omicron variant and currently there are 10 patients in hospitals across England (ages 18 to 85) diagnosed with this variant. Despite not disclosing age, vaccination status or any underlying conditions of the person who died, chances are this death is the first in the world to be officially tied to the new variant. The reaction to the news was immediate on the trading floors, as the world major indexes turned to red. While many reports attributed the bearish session to the FOMC meeting and/or the option expiry date, which would take place this Friday, the plummeting by the travel related stocks demonstrated that Covid was the main reason. As observed in Figures 8 and 9, the “JETS” and “AWAY” ETFs plummeted -3.65 and -3.91%, respectively.

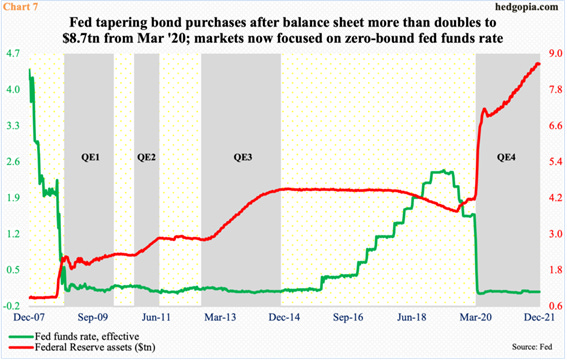

The first two trading days of the week were characterized by investors preparing for a faster US tapering process and thus expecting the Fed to hike rates several times throughout 2022 (Refer to Figure 10). JPMorgan, NatWest Markets, Citi, and Morgan Stanley expect the tapering to conclude by March Q1 2022 (vs. Q2 2022 prev.). This narrative has been gaining momentum in the last weeks, especially when J. Powell admitted inflationary risks to have increased. Jabaz Mathai, Chief Interest Rates Strategist at Citi stated that Wednesday’s FOMC meeting could be an opportunity for the Fed to fight inflation, which significantly exceeds its target. Figure 11 shows the Fed balance sheet currently accounting for $8.7 trillion in assets, more than twice with respect to March 2020. By applying the previous bond purchase pace of $15 bn per month, the balance sheet will grow to $9 trillion by mid-2022. Meanwhile, the zero-interest-rate bound has been the norm for benchmark rates since the pandemic started. If we analyse the futures market, investors are currently pricing more than a 90% chance of a quarter-point tightening by May next year a completely different guidance from that of the Fed. At the same time, US 10Y futures negative momentum persists after net shorts have reached their highest since February 2020. On Monday the US 10Y Yield accounted for slightly less than 1.5%, which cumulates a decrease of 25 bps since its 5-month high of 1.7%. When it comes to the greenback, its net long positions reached the highest since mid-June 2019 after 21 consecutive weeks cumulating bullish momentum despite the unfavourable seasonality on the last trading month of the year. Since September’s FOMC Meeting, when the Fed announced the possibility of the tapering process initiating from November onwards, the USD has appreciated 3.3%. In my opinion, the USD is significantly overvalued. Nevertheless, the greenback may soar further as the ECB and the BoJ will hike rates more slowly than the Fed.

The same day before the FOMC meeting, US retail sales showed a cooling down in consumer sentiment (See Figure 12). Accounting for 0.3% (vs. 0.8% exp.), US retail sales increased less than expected in November, suggesting that the economy may not be ready for a rate hike as growth would be one of the main collateral damages. As a matter of fact, JPMorgan observed the consumers’ expenditures significantly weakened during the last weeks compared to prior years and according to their forecasts of the Chase cards they expect December to be a weaker-than-expected month. Conversely, the inflationary pressure has soared again after the US PPI reading showed an increase of 9.6% YoY (vs. 9.2% exp.), the highest since 2010 (Refer to Figure 13). When it comes to Core PPI, which excludes food and energy, it soared 7.7 YoY (vs. 7.2% exp.). Businesses’ COGS have sharply increased in the last months as a consequence of increasing transportation bottlenecks, strong demand and labour restrictions, which in turn has forced companies to pass these increased costs to consumers by increasing prices. According to Bloomberg, higher US CPI readings are expected in the next months.

From the FOMC meeting minutes, I would highlight several takeaways. First, the Fed doubled the pace of the tapering from $15bn to $30bn per month. Thus, as the markets had already priced, the asset purchase process will end in March 2022. Second, they also stopped using the word “transitory”, something Powell had already admitted some weeks ago. Powell also left the door open to multiple interest rate hikes in the next year after stating that the gap between the end of the tapering and the first-rate hike may be close to each other. But if there is something that shook markets, that was the Fed’s confirmation of interrupting the rate hike in case the growth prospects significantly deteriorated in the next months. For this reason, as soon as this sentence was mentioned, the main three US indexes (S&P 500, NASDAQ and Russell 2000) initiated a bull run and closed the Wednesday trading session with +1.57%, +2.29%, and +1.56% respectively (Refer to Figures 14, 15 & 16). This was already predicted by Charlie McElligott, who stated that unless the Fed “surprised” markets, he saw the risk/reward trade as favourable during the next 2-4 weeks when a substantial amount of notional could be bought after Friday’s expiry date. He also observed that investors are covered against 3-sigma events with the options SPX 3m Skew at the 96th percentile and the 3m Put Skew at the 94th percentile, both at the highest since 1996. The immediate reaction of the Treasuries was to undo their hedging as a result of the strong spike in the major indexes. Similarly, the greenback did not fluctuate much from what investors had already discounted. Finally, the Fed forecasts that inflation will run at 2.6% by December 2022, a projection that substantiated Wednesday’s bull run. After the FOMC meeting, Goldman Sachs published its forecasts in which three interest rate hikes can be observed – May 2022, July 2022, and November 2022 – (Refer to Figure 17). As analysed in #11 Weekly Market Updates, my take is that the Fed will make a policy mistake if they hike rates given their limited margin of safety to do so. This is not the first-time markets witness policy mistakes. Rather, they have occurred several times during the last years and, as observed in Figure 18, the consequence (apart from being forced to cut rates back) is quite unfavourable to most of the major asset classes, especially equities.

UK’s CPI hits 5.1%, climbing to a 10-year high, the BoE reacts by hiking rates to 0.25% for the first time in three years

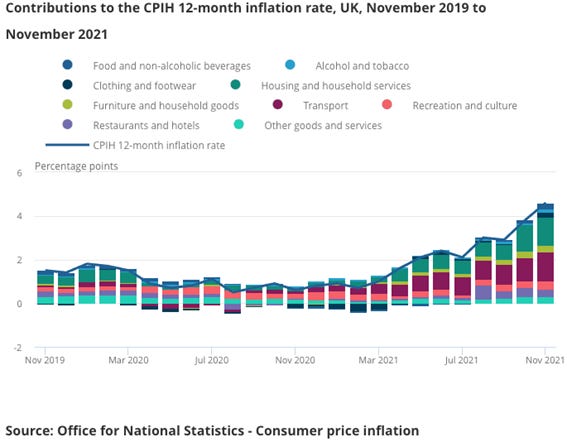

On Thursday morning, the Office for National Statistics released the UK’s CPI data for November 2021. Accounting for +5.1% YoY and beating forecasts of +4.7%, the reading showed a 10-year high, putting the BoE against the ropes after they denied raising interest rates on the prior meeting. As we can see in Figure 19, the largest contribution came from transport with 1.34% as a result of the increasing prices of gasoline and used vehicles (Refer to Figure 20). As a matter of fact, the IMF had warned the BoE not to delay the rate hike in the face of high inflation. It did not take long until the BoE decided to increase rates by 0.15%, to 0.25% after a majority of 8-1. The Committee also voted unanimously to maintain the stock of asset purchases at £895bn. Bank staff expect inflation to remain around 5% through most of the winter period, and to peak at around 6% in April 2022. The CPI inflation is still expected to fall back in the second half of 2022. On that same day, the President of the ECB, Christine Lagarde announced that the ECB will conduct the net asset purchases under the Pandemic emergency purchase programme (PEPP) at a slower pace than in the previous quarter and it expects to discontinue the purchases by March 2022. When it comes to the asset purchase programme (APP), the ECB announced a monthly net purchase pace of 40€bn in Q2 2022 and 30€bn in Q3. From October 2022 onwards, net asset purchases will shift back to 20€bn for as long as necessary to reinforce the accommodative impact of its policy rates (Refer to Figure 21). They expect net purchases to end shortly before the ECB starts raising rates, which will remain unchanged throughout the entire 2022. The meeting concluded with the ECB’s inflation’s forecasts of 3.2% as of December 2022. Despite being slightly more realistic than that of the Fed, these expectations seem to be far from reality as inflationary pressures keep rising in Germany, whose PPI for November has reached a 56-year high increasing 19.2% YoY (See Figure 22). Despite energy prices have been the main contributor, there are no signs showing inflation to cool down in the next months. As daily cases keep increasing and the ongoing pessimistic macro scenario remains, the growth projections are constantly being adjusted. One of the latest central banks to take the lead has been the Bank of Spain, which has cut its growth forecast for 2021 to 4.5% (from 6.4% prev.) and 5.4% in 2022 (vs. 5.9% prev.). As a result, the GDP would break-even to pre-pandemic levels by 2023, a year in which the unemployment rate would account for 12.9% (vs. 13.3% prev.). As for inflation, the Bank of Spain describes inflationary pressures as one of the biggest threats ahead. Being less optimistic than its counterparts, it expects inflation to hit 3.7% by December 2022 and it would not be until 2023 that it would fall below the 2% target with a reading of 1.2% (Refer to Figure 23).

Everything happens for a reason: The option expiry date

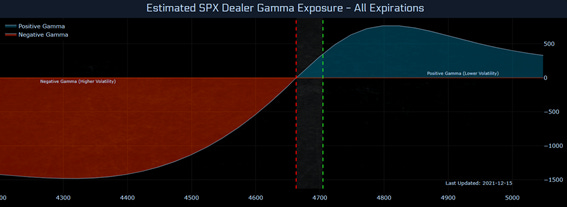

Undoubtedly, the session with the capacity to influence the behaviour of markets was Friday’s options expiry date. After three of the most influential central banks had concluded their scheduled meetings, the typical turbulences before the Op-Ex have been magnified because of the low liquidity. As a result, VIX has soared 11.59% during this week (-30.69% MTD), a pattern we have been witnessing on every option expiry date (See Figure 24). As observed in Figure 25, positive gamma prevails, which translates into less volatile sessions or, said in other words, candles in technical charts should be narrower. Thursday’s session after the intervention of the BoE and the BCE, we witnessed some contradictory reactions. First, the SPX rebounded exactly on the $4,642 technical level, which is the flip dealer point, or, to put it simply, the point in which the gamma shifts from negative to positive and vice versa. Moreover, there was a massive exodus from unprofitable tech and software companies with an EV/Sales ratio of at least 8x, with losses of 5.37% and 4.83%, respectively (Refer to Figure 26). Consequently, the e-mini NASDAQ future reported a loss of 2.58%, after investors rebalanced their portfolios before Friday’s session, after which liquidity tends to drain significantly. As a matter of fact, by observing the $RSP, which equally weights all the components of the S&P 500, we can confirm the extreme influence of tech on US major indexes ($RSP performance on 15/12/2021 = -0.18%). Similarly, the Dark Pool Index shows buying divergence, providing further evidence of the broad market momentum and indicating institutional investors are not selling (See Figure 27). Another inconsistency spotted during the session was the appreciation of the EUR against the USD, especially after the BCE announced no rate hikes expected during 2022. Moreover, crude oil, which used to be positively correlated with equities, soared 1.81%.

Lombard Odier considers Chinese real estate a systematic risk

The Swiss private bank specialising in wealth and asset management, Lombard Odier, has recently published a report in which outlines the worrying situation in China after the default of two of its biggest developers, Evergrande and Kaisa. According to them, the slowdown on the Chinese property market was a by-product of the CPC tightening the real estate regulation at the beginning of the year. By then, the CPC emphasized its ambition to realign the real estate sector, claiming that “housing is for living and not for speculation”. After the Chinese government issued more than 400 new regulations (including curbs on mortgages and bank loan disbursements) property affordability was pushed down for the middle class in urban areas. To put things in perspective, a mortgage could be obtained in around one month. After the regulations, this process now takes up to six months. It was then that property companies started to be placed in a life and death situation. As of this writing, the Swiss private bank believes there is a 30% default rate in the offshore USD China high yield real estate market, which means that what started as an idiosyncratic risk has now become a systematic one. They also estimate that a 10% reduction in construction equates to a 2% loss in GDP. As analysed in #12 Weekly Market Update, the Chinese real estate sector is worth USD 60 trillion, encompassing 60% of household wealth and representing up to 30% of the country’s GDP both directly and indirectly. Last week, the Chinese government announced that they would loosen some of their restrictions and, similarly, the PBoC cut its reserve requirement ratios. The second conclusion of the report is that the risk of contagion is being taken seriously by Chinese authorities. As we can observe in Figure 28, which plots the Evergrande’s yield (LHS) and the Chinese CDS (RHS), the decrease in the latter after the former soared indicates that investors seem to be regaining their faith in the Chinese government, which is currently trying to cushion this risk. They expect authorities to implement new policies which reduce stress for real estate developers for them to obtain funding at reasonable and sustainable yields. Once the pressure is eased, higher-quality debt may rally from current stressed and elevated yield levels. Nevertheless, as of this writing the negative sentiment towards China prevails. This week, David Ingles, one of the leading APAC reporters from Bloomberg has observed that the Hang Seng Index is currently trading below book as its price-to-book ratio has reached 0.99, a level which may trigger contrarian reactions. (Refer to Figure 29).

Goldman remains bullish on crude oil

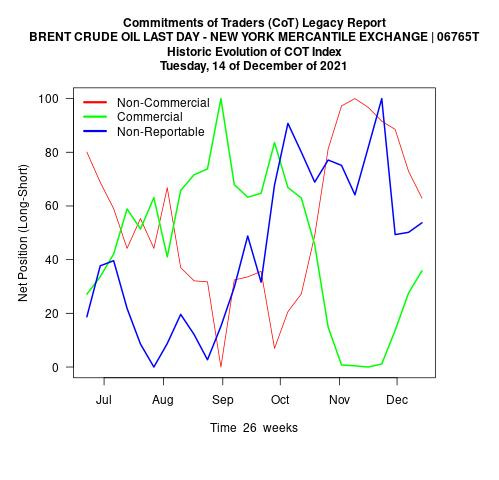

Despite WTI Crude oil having plummeted by 18% from November’s high, Goldman released a report expecting the black gold to reach $100 per barrel by 2023 as, according to them, supply additions are expected to be too slow to keep up with record demand. The bank sees the recent sell-off as overdone on unnecessary concerns about omicron-related restrictions and expects investors to buy the dip once asset managers reallocate their money in early 2022 (Refer to Figure 30). Figure 31 shows the evolution of the Commitment of Traders (CoT)’s bets on Brent Crude Oil.

Turkish lira plummets after the Turkish central bank cuts rates

The Turkish President, Tayyip Erdogan has been responsible for another Turkish drama blockbuster. As analysed in previous Weekly Market Updates, Turkey’s CPI for October showed an increase of 20% YoY, a level last seen in the wake of a currency crisis three years ago. The November reading showed further inflation pressures with an increase of 21.3% YoY. This week, Erdogan has replaced two (more) deputy finance ministers and right after Turkey’s central bank cut rates again for the third month in a row, driving the currency’s real yield well below zero (Refer to Figure 32). This has brought about the TRY to tumble to another record low, falling the psychological barrier of 15 TRY/USD for the first time. The bank is also expected to reduce the one-week repo rate by 100 bps to 14%, well below inflation (21.3%). With the economy already destabilized, Turkey currently cumulates $446bn of gross external debt and the MSCI Turkey ETF has reached an all-time low at $16.97 (See Figure 33). Similarly, the yield on the 10Y government bonds soared 57bps, the biggest increase since September.